When you apply for a loan, credit card, or even an EMI plan, lenders often look at one number before making a decision and that’s your credit score. This three-digit figure tells banks how trustworthy you are as a borrower.

Yet, many people still wonder: What is a credit score, how is it calculated, and why does it matter so much?

Here’s a beginner-friendly guide explaining everything you need to know.

What Is a Credit Score?

A credit score is a three-digit number that reflects your creditworthiness. In simple terms, how likely you are to repay borrowed money on time.

It is calculated by credit bureaus using your financial behaviour, such as how you handle loans, EMIs, and credit cards.

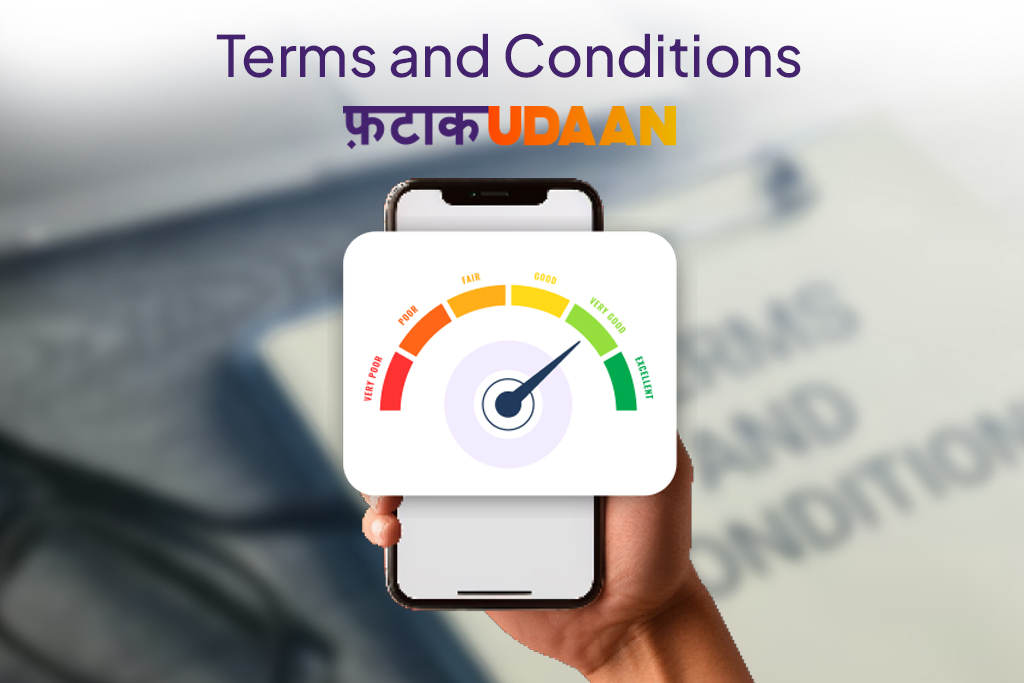

Typical credit score range in India:

- 300–579: Poor

- 580–669: Fair

- 670–739: Good

- 740–799: Very Good

- 800+ : Excellent

A higher score makes it easier to get loans, credit cards, lower interest rates, and faster approvals.

How Credit Scores Are Used

Banks, NBFCs, and digital lenders rely on credit scores to make decisions such as:

✔ Loan Approval

A good score increases the chances of getting approved instantly.

✔ Interest Rate Determination

Borrowers with higher scores usually receive better, lower interest rates.

✔ Credit Card Limit Allocation

A better score may help you secure higher limits.

✔ EMI Tenure and Loan Amount

Lenders offer longer tenures and bigger loan amounts to borrowers with strong credit profiles.

✔ Risk Assessment

A poor score signals higher risk, leading to rejections or stricter terms.

How Credit Scores Are Calculated

Credit bureaus analyse several aspects of your credit behaviour. Here are the key factors:

1. Repayment History (35%)

Timely EMI and credit card payments have the biggest impact.

2. Credit Utilisation Ratio (30%)

Using too much of your credit limit can reduce your score.

3. Credit Mix & Types (10%)

Having both secured and unsecured loans helps build a balanced profile.

4. Length of Credit History (15%)

The longer you’ve held accounts, the better.

5. New Credit Enquiries (10%)

Too many loan applications in a short time can lower your score.

Different Credit Scoring Models

India has multiple credit bureaus, each with its own scoring method:

✔ CIBIL Score (Most Widely Used)

Ranges from 300 to 900.

✔ Experian Credit Score

Also ranges between 300 and 900.

✔ Equifax & CRIF Highmark

Use similar scoring models based on repayment patterns and credit activity.

Although scores may differ slightly across bureaus, the underlying assessment criteria remain largely the same.

What Is a Good Credit Score?

A good credit score in India typically starts from 700 and above.

- 700–749: Acceptable for most loans

- 750–799: Strong financial credibility

- 800+ : Excellent and highly trusted by lenders

The higher your score, the easier it becomes to secure instant personal loans, negotiate better terms, and enjoy faster approvals.

Why Credit Awareness Matters More Than Ever in 2026

Lending becomes faster and increasingly digital in 2026, your credit score is often the first filter lenders use to assess eligibility. From instant personal loans and BNPL options to app-based EMIs, a strong credit profile now plays a central role in accessing everyday financial products. Staying credit-aware and monitoring your score regularly helps you stay prepared for opportunities while avoiding surprises during approvals.

How Can You Increase Your Credit Score?

Improving your credit score is absolutely possible with consistent habits:

1. Pay all EMIs and credit card bills on time

Even one missed payment can reduce your score.

2. Keep your credit utilisation below 30%

Low utilisation signals disciplined financial behaviour.

3. Avoid multiple loan applications

Too many enquiries can make lenders see you as high-risk.

4. Maintain older credit accounts

Longer credit history improves your profile.

5. Regularly check your credit report

Identify and dispute any inaccuracies immediately.

6. Take small loans & repay on time

This helps build a positive repayment track record.

Check Your Credit Score & Improve It with FatakPay

Your credit score is the key to unlocking better financial opportunities.

Check your credit score for free on the FatakPay app and start building a stronger credit profile today!

FAQs

1. What is the meaning of a credit score?

It’s a three-digit number that shows how reliably you can repay borrowed money.

2. What is considered a good credit score?

A score of 700+ is generally seen as good and increases your chances of loan approval.

3. How often should I check my credit score?

Once every 3–6 months is recommended, or before applying for a loan.

4. Does checking my credit score reduce it?

No. Soft enquiries (self-checks) do not impact your score.

5. Can I improve a low credit score?

Yes, with good repayment habits, lower credit utilisation, and disciplined borrowing.

| Instant Loans by Amount | |||

|---|---|---|---|

| ₹1500 Instant Loan | ₹2500 Instant Loan | ₹5000 Instant Loan | ₹10000 Instant Loan |

| ₹12500 Instant Loan | ₹15000 Instant Loan | ₹17500 Instant Loan | ₹20000 Instant Loan |